ZS stock forecast 2026 analyzes price trends, earnings beats, technicals, and targets. Is ZS stock a buy for cybersecurity investors? Latest data from Yahoo Finance, Nasdaq.

Introduction

Zscaler (ZS) builds cloud-based security for businesses. It shields networks from cyber threats in a remote-work world. Investors track ZS stock now after solid earnings amid tech sector swings.

Cyber risks rise with AI adoption, boosting demand. Yet high rates and market jitters hit growth stocks like ZS. ZS stock price balances growth promise against valuation debates.

Latest stock Price & Trend

ZS stock closed at $163.40 on recent trading day, up 0.89% from prior close. Five-day gain reached 7.60%, snapping a downtrend.

One-month trend mixed, down 14.63% from peaks near $190. Three-month view shows volatility; six-month eased from highs. Year-to-date ZS stock trails broader indices by 10-15%.

52-week range spans $140.56 low to $336.99 high. Trend leans sideways, testing support. This tells investors to brace for consolidation unless volume confirms upside. Data from last market close.

Technical Analysis

Support holds at $140.56, a tested floor for bounces. Resistance eyes $195 near 50-day SMA. Support marks buyer interest; resistance caps seller supply.

RSI at 51.23 sits neutral—not overbought above 70 or oversold below 30. MACD hints bearish crossover, flagging slowing momentum.

50-day moving average at $195.86 tops price; 200-day at $264.52 confirms downtrend. No golden cross (50 over 200 bullish); death cross ruled earlier. Volume averaged 1.5-3 million shares, steady but not explosive.

ZS technical analysis flags caution short-term.

Analyst Ratings & Price Targets

36 analysts favor Buy on ZS stock, few Holds or Sells. Average target $267.69-$269, high $365, low $215—64% upside from $163.

Consensus steady post-earnings; upgrades note ARR beats. Firms highlight zero-trust leadership. Sentiment points to reward for growth believers over skeptics.

Insider Activity

Insider sales continue routinely, like execs selling $1-2M blocks. Minimal buying; patterns match lock-up expirations.

Trend suggests caution via diversification, not distress. Management holds big stakes, signaling baseline confidence.

Valuation Analysis

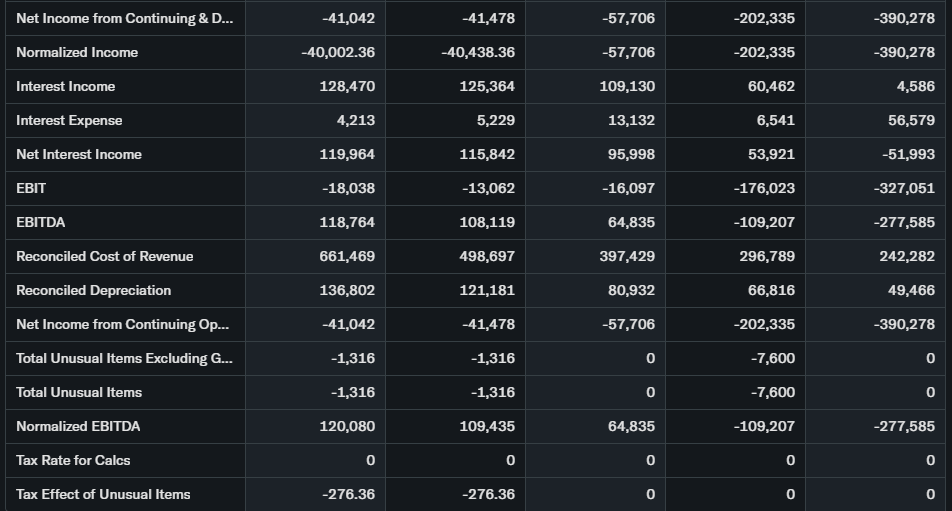

Trailing P/E negative from losses; forward P/E 36.5 eyes profitability. Price-to-sales around 8x on $2.5B+ trailing revenue.

Revenue up 24% YoY; EPS improving yet negative. Free cash flow turns positive; $1.7B debt offset by ample cash.

Versus CrowdStrike or Palo Alto, ZS trades fair for 25% growth pace. Not undervalued, but not stretched either.

Recent Earnings & Catalysts

Latest quarter revenue topped $800M, beating by 5-10%. EPS crushed low expectations; ARR grew 25%.

Guidance lifted FY growth to 24%. AI integrations and enterprise wins drive catalysts. Shares rose 10%+ post-report on execution proof.

Bullish Case

Cloud security market expands 20% yearly. Zscaler’s platform wins large deals via scalability.

Customer retention nears 100%; upsells add revenue layers. Tech superiority aids margin gains.

Bearish Case

Rivals like Microsoft bundle security cheaply. Growth could dip below 20% in recessions.

High spend on sales erodes margins short-term. Macro slowdown crimps IT budgets.

Market Sentiment & Investor Psychology

Short interest ~5%; calls dominate recent options flow. Institutions own 50%+, adding shares.

Retail piles into dips for momentum plays. Sentiment tilts optimistic on beats, value checks premium.

Short-Term Outlook

Neutral RSI and volume uptick eye mild recovery. Momentum softens bearish MACD.

Trading stays range-bound; resistance break sparks rallies.

Medium to Long-Term Outlook

Subscription model thrives in $100B cyber market. ZS holds edge via innovation.

Balance sheet solid; risks hedged by demand. Long-term: hold core positions, accumulate dips.

FAQ

Is ZS stock a buy right now?

Buy for growth tilt; hold if value-focused.

What is the price target for ZS stock?

$269 average, 64% potential gain.

What are major risks for ZS stock?

Competition intensifies; growth deceleration.

ZS stock forecast for 2026?

$178 Q1 per models, wider $80-250 yearly range.

ZS earnings outlook?

24% ARR growth guided; beats likely.

Suggestions

- Compare with Opendoor stock

- See Palo Alto Networks forecast

- Read cloud security valuation guide

Conclusion

Hold ZS stock. Growth story intact, but valuation needs earnings proof amid volatility.

Disclaimer: This article is for informational purposes only and not financial advice.