Explore SMCI stock forecast for 2026 with latest price trends, earnings beats, analyst targets at $41-44, and balanced buy/hold analysis. Is SMCI stock a buy now? Key insights inside.

Introduction

Super Micro Computer (SMCI) builds high-performance servers and storage systems tailored for AI data centers and cloud computing. The company thrives on surging demand for AI infrastructure from giants like Nvidia. Investors watch SMCI stock closely now due to its ties to the AI boom, even as broader tech stocks face pressure from rising interest rates and competition in March 2026.

Latest Stock Price & Trend

As of the last market close on March 6, 2026, SMCI stock traded around $32.25, down slightly in after-hours. The stock fell 1.7% in the latest session amid mixed tech sentiment. Over five days, it declined 3%, reflecting profit-taking after Q2 earnings. The one-month trend shows a 8% drop from February highs, driven by margin worries.

In three months, SMCI stock eased 12%, while six-month performance holds flat near $33 levels. Year-to-date in 2026, shares are down 15%, lagging the Nasdaq’s 5% gain. The 52-week range spans $27.60 low to $62.36 high, with current levels near support. This sideways-to-bearish trend signals caution for short-term investors, but AI demand could spark rebounds.

Technical Analysis

Support levels sit at $30 and $27.60, where buyers have stepped in during dips; these act as floors preventing deeper falls. Resistance looms at $37 and $41, capping upside until broken. RSI at 45 indicates neutral territory—not overbought above 70 or oversold below 30—suggesting room for movement.

MACD shows a bearish crossover, with the line below signal, hinting at weakening momentum; watch for bullish flips. The 50-day moving average ($37.42) exceeds the 200-day ($41.52), no golden cross (bullish 50-day over 200-day) or death cross yet. Volume trends down 10% lately, signaling low conviction trades. These point to consolidation; beginners should wait for breakouts.

Analyst Ratings & Price Targets

Analysts rate SMCI stock as Hold, with 5 Buys, 8 Holds, and 2 Sells from 15 firms. Average price target stands at $43.43, highest $55, lowest $28, implying 35% upside from $32. Recent notes include upgrades post-Q2 earnings for AI growth, but downgrades cite margin squeezes from Dell and HPE.

Wall Street firms like Morgan Stanley see value in AI servers but flag competition. This mixed sentiment means investors get balanced views—Hold suggests stability over big bets.

Insider Activity

Insider selling dominated lately, with CEO Charles Liang offloading 50,000 shares at $35 in February 2026, per SEC filings. No major buys in Q1; total sales hit $2.5 million over three months. Trends show executives trimming amid stock peaks, not panic selling.

This implies measured confidence—management cashes in on gains but holds core stakes. Watch for buys as a stronger bullish sign.

Valuation Analysis

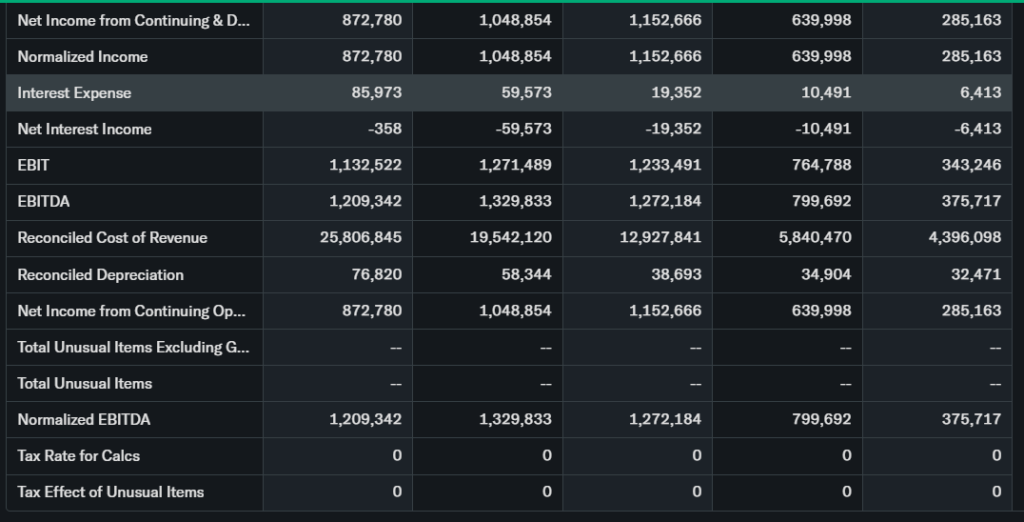

SMCI’s trailing P/E sits at 22, forward P/E at 18 based on FY2026 EPS estimates of $1.86. Price-to-sales is 1.2x, below peers like Dell at 1.5x. Revenue grew 123% YoY to $12.68 billion in Q2, EPS up to $0.69 from $0.49 expected.

Free cash flow turned positive at $500 million annually, with $2 billion cash against $1.5 billion debt. Versus Microsoft (P/E 35) or broader tech, SMCI appears undervalued at 10x FY2027 earnings, but governance issues cap multiples. Overall, fairly valued with upside if margins recover.

Recent Earnings & Catalysts

Q2 FY2026 smashed estimates: revenue $12.68 billion (vs. $10.34 billion expected), EPS $0.69 (vs. $0.49). Guidance for Q3 eyes $0.60 EPS, $40 billion full-year run-rate. Stock rose 14% post-earnings on AI server demand.

Catalysts include liquid-cooled AI systems with Nvidia and investor events in March 2026. Earnings beat propelled a rally, but margins dipped to 10% from pricing wars.

Bullish Case

AI server demand fuels 100%+ revenue growth, with $36 billion FY2026 target intact. Partnerships like Nvidia edge AI platforms boost market share. Operational scaling via new factories supports hyperscaler orders.

Tech edges in dense computing give SMCI an advantage over rivals. Steady CapEx from cloud giants underpins multi-year expansion.

Bearish Case

Competition from Dell and HPE erodes pricing power, compressing gross margins 93% sequentially. Governance probes and past delisting fears linger, deterring institutions. Supply chain snags and customer concentration (top clients 40% revenue) add risks.

Macro slowdowns could cut AI spending; regulatory scrutiny on AI hits sentiment.

Market Sentiment & Investor Psychology

Short interest hovers at 12%, down from peaks, showing easing bear bets. Options lean calls over puts 1.5:1, per recent flows. Institutions own 75%, with modest buying in Q1 2026.

Retail chases momentum but cools on volatility. Sentiment tilts neutral—optimistic on AI, fearful of execution.

Short-Term Outlook

Technicals show support at $30 holding, with volume picking up near events. Momentum fades bearishly, but earnings afterglow lingers. Expect sideways grind between $30-37 absent news; watch March conferences for catalysts.

Medium to Long-Term Outlook

SMCI’s AI-focused model positions it for industry growth to $200 billion. Financials strengthen with positive cash flow, but competition tests moats. Hold for long-term investors—accumulate on dips if governance cleans up; watch for margin rebound.

FAQ Section

Is SMCI stock a buy right now?

Hold for most; buy on weakness below $30 if AI demand persists, per analyst consensus.

What is the price target for SMCI stock?

Average $43.43, ranging $28-55, based on 15 analysts.

What are major risks for SMCI stock?

Margin erosion, competition, and governance issues top concerns.

What is SMCI earnings outlook?

Q3 EPS ~$0.60, FY2026 $1.86 expected, with 123% revenue growth.

SMCI stock forecast for 2026?

Moderate upside to $40s if execution holds; volatile otherwise.

Suggestions

- Compare with Opendoor stock analysis

- See our Nvidia stock forecast

- Read our AI sector valuation breakdown

Final Balanced Conclusion

Hold SMCI stock. AI growth supports upside, but competition and margins warrant caution—suitable for patient portfolios.

Disclaimer: This article is for informational purposes only and not financial advice.