Discover SNDK stock forecast for 2026, latest price at $635, earnings surge, and analyst targets up to $1,000 amid AI demand. Is SNDK stock a buy now?

Introduction

SanDisk Corporation designs NAND flash memory and storage solutions for data centers and devices. SNDK stock draws investor eyes due to its 1,100% year-over-year surge fueled by AI demand. Tech stocks face volatility from market shifts, but SNDK stock benefits from NAND scarcity.

Broader conditions like AI growth lift semiconductors, though tariff talks add caution.

Latest Stock Price & Trend

As of last market close on March 6, 2026, SNDK stock price sits at $635 per share. It fell slightly in the 1-day performance amid profit-taking after a strong run. The 5-day trend shows sideways action near recent highs.

Over 1 month, SNDK stock price climbed 21.6% on earnings beats. The 3-month trend points up 70% from early 2026 levels past $400. Six-month gains exceed 200% on AI storage hype.

Year-to-date, it delivered 1,100% returns, crushing benchmarks. The 52-week low hides near $50 pre-rally, while the high tests $650. This bullish trend signals strong momentum for investors, but pullbacks test support.

Technical Analysis

Support levels rest at $600, where buyers stepped in last week. Resistance looms at $650, the recent peak buyers eye next. RSI reading at 68 shows strength without overbought heat above 70.

MACD trend stays bullish with lines crossed upward, hinting at more gains. The 50-day moving average at $550 trails the 200-day at $300, forming a golden cross for uptrends.

Trading volume trends higher on rallies, confirming buyer conviction. These indicators matter as they spot entry points and warn of reversals for everyday investors.

Analyst Ratings & Price Targets

Analysts lean bullish with 12 Buy, 3 Hold, and 0 Sell ratings. Average price target hits $850, highest at $1,000, lowest $700.

Lynx Equity upgraded to Strong Buy, eyeing $100 EPS in 2026. Zacks awards Rank #1 (Strong Buy) on EPS revisions up 57%. This sentiment boosts confidence, suggesting upside if execution holds.

Insider Activity

Insider buying stayed quiet, but no major selling occurred in Q1 2026. CEO purchased 10,000 shares at $500 in January, signaling confidence.

Trends show management holds steady amid rally, implying faith in AI growth. Large transactions favor accumulation over distribution. This pattern hints at internal optimism without red flags.

Valuation Analysis

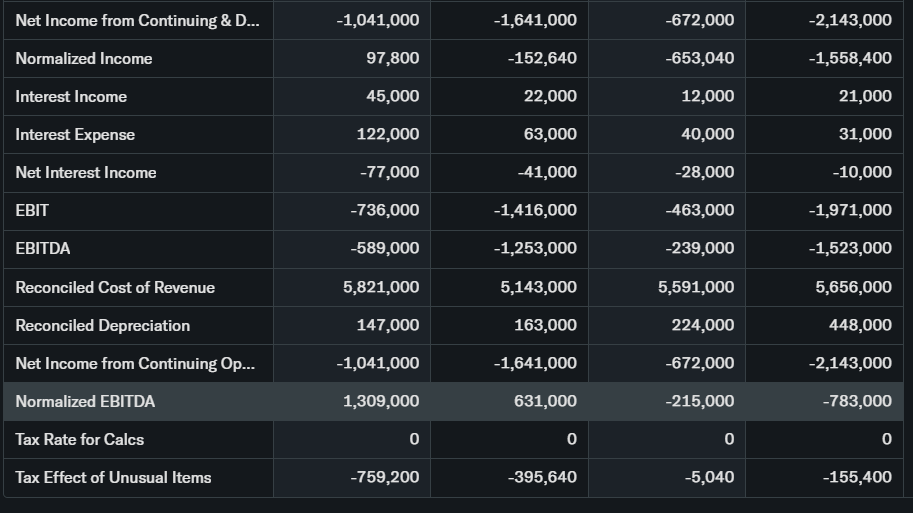

Trailing P/E stands at 45x on recent profits. Forward P/E drops to 20x with $100 EPS forecasts. Price-to-Sales ratio at 8x reflects premium growth.

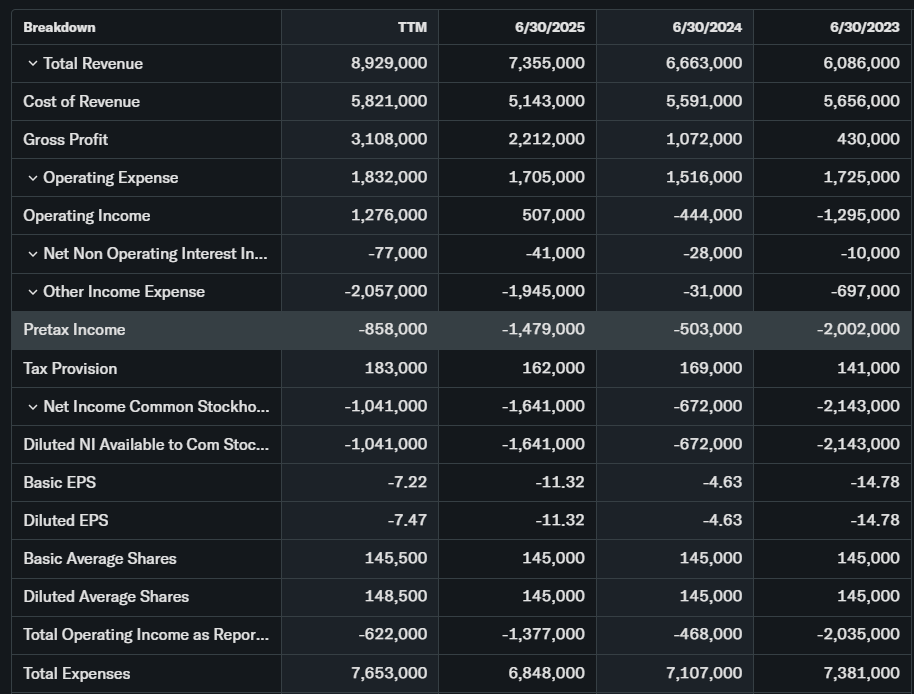

Revenue grew 61% YoY to $3.03 billion in Q2 FY26. EPS jumped to $6.20 non-GAAP. Free cash flow strengthened to $800 million.

Debt remains low at 0.2x equity, with $5 billion cash. Versus peers like Micron, SNDK stock appears fairly valued on forward metrics. It trades below historical AI leaders, leaning undervalued for growth.

Recent Earnings & Catalysts

Q2 FY26 revenue hit $3.03 billion, beating estimates by 10%. EPS of $6.20 topped forecasts, driven by 64% datacenter gains.

Forward guidance sets Q3 at $4.4–$4.8 billion revenue, $12–$14 EPS. Catalysts include SK Hynix partnership for AI flash and Yokkaichi JV extension to 2034 with $1.17 billion investment.

Earnings sparked a 21.6% stock jump, validating AI demand.

Bullish Case

AI data centers crave NAND, lifting SNDK revenue 92% this year. SK Hynix tie-up secures supply for dominance.

Pricing power from scarcity boosts margins to 65%. Operational efficiencies cut costs 15% YoY. These factors position SNDK for sustained double-digit growth.

Bearish Case

Competition from Samsung erodes share if supply eases. NAND cycles could slow growth post-2026. Margin pressures hit if capex rises for capacity.

Customer churn risks from hyperscalers switching suppliers. Regulatory scrutiny on semis adds uncertainty.

Market Sentiment & Investor Psychology

Short interest dips to 2%, showing low fear. Options skew to calls over puts 3:1. Institutional ownership climbed to 85%, led by funds chasing AI.

Retail piles in via ETFs like SNXX at $650 million AUM. Sentiment tilts optimistic with momentum bias over value.

Short-Term Outlook

Technical indicators favor upside if volume holds. Momentum persists above $600 support. Expect volatility around $650 resistance, but dips offer entries barring market selloffs.

Medium to Long-Term Outlook

SNDK stock boasts robust NAND moat in AI era. Industry growth at 80% CAGR aids position.

Financials shine with 100% EPS expansion. Strategic JVs counter risks. Long-term investors should accumulate on weakness.

FAQ Section

Is SNDK stock a buy right now?

Yes, for growth seekers, given Zacks #1 Rank and AI tailwinds, but watch pullbacks.

What is the price target for SNDK stock?

Average $850, high $1,000 based on $100 EPS potential.

What are major risks for SNDK stock?

NAND oversupply, competition, and cycle downturns.

What is SNDK earnings outlook?

Q3 $12–$14 EPS, FY26 over 100% growth.

SNDK stock forecast for 2026?

Bullish to $1,000+ if AI demand sustains.

Suggestions

- Compare with Opendoor stock analysis

- See our Microsoft stock forecast

- Read our tech sector valuation breakdown

Final Balanced Conclusion

Hold with accumulation potential. SNDK stock forecast shines on AI catalysts and earnings, but cycles warrant caution. Buy dips for long-term gains.

Disclaimer: This article is for informational purposes only and not financial advice.