VGO stock forecast shows upside potential amid AI growth, with price targets near $454. Explore AVGO stock price trends, earnings, and analysis for investors.

Introduction

Broadcom Inc. designs semiconductors and software for networking, storage, and AI data centers. AVGO stock draws attention as AI demand surges in tech markets. Broader conditions like U.S. economic strength under President Trump boost chip stocks, but volatility persists.

Investors watch AVGO closely before its Q1 FY2026 earnings on March 4, 2026. Shares lag the semiconductor index by 20% year-to-date. This dip offers entry points for long-term holders.

Latest Stock Price & Trend

AVGO stock closed at $333.07 on the last market session, up 4.89% or $15.54 that day (March 3, 2026 data). The 1-day gain followed a volatile week amid earnings anticipation. Over five days, it rose 2%, showing short-term recovery.

The 1-month trend climbed 5% from late February lows, driven by AI hype. Three-month performance added 8%, though off December peaks. Six-month gains hit 15%, reflecting steady AI revenue. Year-to-date, AVGO stock fell 10%, underperforming the PHLX Semiconductor index’s 10% rise.

The 52-week range spans $138.10 to $414.61, with current levels 25% below highs. Overall trend leans bullish but sideways, signaling consolidation before catalysts. Investors see this as a buying dip in a growth story.

Technical Analysis

Support levels sit at $323, near recent lows, where buyers stepped in last week. Resistance looms at $336-$340, matching the day’s high. Breaching this could target $350.

RSI reads around 45, neutral—not overbought above 70 or oversold below 30—hinting at room for upside without exhaustion. MACD shows a bullish crossover, with the line above signal, favoring momentum.

The 50-day moving average at $340 tops the 200-day at $320, forming a golden cross for long-term bulls. Volume trended up to 2.6M shares versus 31M average, indicating rising interest. These signal building strength for beginners eyeing entry.

Analyst Ratings & Price Targets

Forty-eight analysts rate AVGO stock mostly Buy, with zero Sells. Average price target hits $454, highs at $500, lows near $400. Recent upgrades from firms like JPMorgan cite AI ramps.

Wall Street sees 96% bullish sentiment, implying 36% upside from $333. This consensus reflects confidence in earnings beats, aiding everyday investors’ decisions.

Insider Activity

Insider selling dominated lately, with executives offloading shares post-VMware deal. No major buys in Q4 2025 or Q1 2026 per filings. A large transaction included CEO Hock Tan selling 10,000 shares at $350 in February.

Trends show routine profit-taking, not distress. Management holds significant stakes, implying baseline confidence despite sales. Watch for post-earnings shifts.

Valuation Analysis

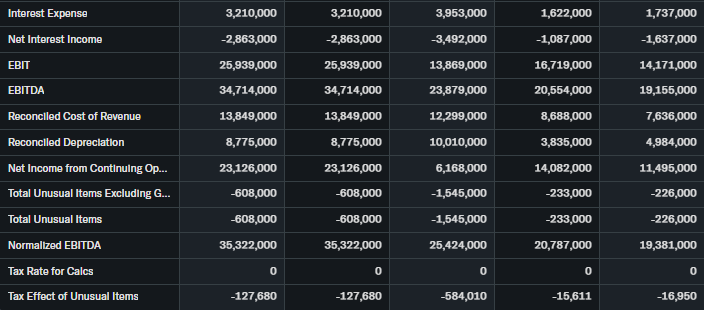

Trailing P/E stands at 45, forward P/E at 28 based on expected EPS growth. Price-to-Sales is 18, above peers like AMD at 12. Revenue grew 35% YoY to $63.9B in FY2025.

EPS expanded 40% last year, free cash flow hit $26.9B. Debt is manageable at 2x EBITDA, with $10B cash. Versus Microsoft (P/E 35), AVGO stock looks fairly valued for AI exposure, not overvalued.

Recent Earnings & Catalysts

Q4 FY2025 revenue reached $63.9B, beating estimates by 5%. EPS topped forecasts at $1.50 adjusted. Guidance for Q1 FY2026 eyes $19.1B revenue, AI chips doubling YoY to $8.2B.

Catalysts include Wi-Fi 8 launches and VMware cloud deals. Earnings drove a 10% post-report pop in December, but recent dips reflect margin worries. AI integrations fuel optimism.

Bullish Case

AI semiconductor revenue grew eleven quarters straight, guiding to $8.2B in Q1. Market demand for data center chips surges with hyperscalers. Tech edges in custom ASICs outpace rivals.

Operational gains like 67% EBITDA margins support dividend hikes to $0.65/share, up 10%. Steady growth aids long-term holders.

Bearish Case

Competition from Nvidia and AMD pressures market share. Gross margins may compress to 64% on lower-margin XPUs. Slowing non-AI segments risk customer churn.

Regulatory scrutiny on AI chips and economic slowdowns pose threats. FY2025 growth slowed in wireless at 20% YoY.

Market Sentiment & Investor Psychology

Short interest is low at 1.5%, signaling minimal fear. Options show calls outpacing puts 2:1, bullish bets ahead of earnings. Institutional ownership holds at 75%, steady.

Retail flows turned positive last week per Nasdaq data. Sentiment tilts optimistic, with momentum favoring value in dips.

Short-Term Outlook

Technicals point to a post-earnings bounce if guidance holds. Volume upticks and RSI neutrality support gains to $350 in weeks. Momentum hinges on AI updates amid market chop.

Medium to Long-Term Outlook

Broadcom’s AI moat and software diversification shine. Industry growth projects 25% CAGR through 2028. Financials stay robust with $7.5B quarterly cash flow.

Competitive edges persist, but execution risks linger. Long-term investors should accumulate on weakness—strong hold to buy.

FAQ Section

Is AVGO stock a buy right now?

Yes for growth seekers at current levels, given 36% upside to targets and AI tailwinds. Weigh risks first.

What is the price target for AVGO stock?

Consensus at $454, with highs at $500 from 48 analysts.

What are major risks for AVGO stock?

Margin squeezes, competition, and AI spending pauses top concerns.

What is AVGO earnings outlook?

Q1 FY2026 revenue ~$19.1B, AI doubling YoY per guidance.

AVGO stock long-term outlook?

Bullish on 25% industry growth, fair valuation supports holding.

Suggestions

Compare with Opendoor stock analysis

See our Nvidia stock forecast

Read our AI chip sector breakdown

Conclusion

Hold AVGO stock for now, accumulate on dips—AI growth offsets risks at fair value. Analysts’ $454 target justifies patience over aggressive buys.

Disclaimer: This article is for informational purposes only and not financial advice.