Explore KVYO stock analysis: latest price, earnings beats, technicals, and forecast. Is KVYO stock a buy amid recent dips? Get valuation insights and outlook now.

Introduction

Klaviyo Inc. (NYSE: KVYO) builds marketing automation software for e-commerce brands. It helps businesses send targeted emails, SMS, and push notifications using customer data.

Investors watch KVYO stock now due to its recent 52-week low and strong Q4 earnings beat. Broader tech sector volatility from economic slowdowns adds pressure on growth stocks like this.

Latest Stock Price & Trend

As of the last market close on March 5, 2026, KVYO stock traded at $20.89. This reflects a 6.5% gain from the day’s low of $19.61 but sits 1.3% below the high of $21.16.

The 1-day performance showed volatility with a 9.2% drop earlier in the week to $15.70. Over 5 days, it rebounded slightly amid earnings reactions.

In the 1-month trend, KVYO stock fell sharply, down about 60% yearly from peaks. The 3-month and 6-month trends mirror this bearish slide despite revenue growth. Year-to-date, it’s down significantly from 2025 highs.

The 52-week high reached around $40 earlier, while the low hit $15.70 recently. This bearish trend signals caution for short-term investors but may offer entry points for long-term ones eyeing fundamentals.

Technical Analysis

Support levels sit near $15.70, the recent 52-week low where buyers stepped in. Resistance looms at $21-22, matching the recent high. These levels matter as they show where price stalls or breaks.

RSI reading hovers oversold below 30, suggesting the stock may rebound as selling exhausts. RSI measures momentum; low values indicate potential buys.

MACD trend shows bearish crossover, with the signal line below zero. This flags downward momentum but watch for reversal if it crosses up.

The 50-day moving average stands above the current price at around $25, while the 200-day is higher near $30. No golden cross (50-day over 200-day) exists; it’s a death cross setup, bearish for now. Moving averages smooth trends to spot direction shifts.

Trading volume spiked on the dip, higher than average, showing strong interest. Rising volume confirms trends, bullish or bearish.

Analyst Ratings & Price Targets

Seventeen analysts rate KVYO stock: 17 Buy, 0 Hold, 0 Sell, a Strong Buy consensus. Average price target is $42.40, with low at $35 and high above.

Recent notes stay positive post-Q4, citing 25-26% growth outlook. No major downgrades noted despite the dip. Wells Fargo and others see value.

This sentiment means Wall Street views KVYO stock as undervalued with upside, good for investors seeking analyst-backed growth plays.

Insider Activity

Insiders sold heavily recently: CEO sold 167,926 shares, total insider sales ~1.51M shares worth $43M in 90 days. Yet insiders own 53.24% of shares, showing skin in the game.

No recent buying noted; sales tie to secondary offerings of 11M shares. This implies caution or profit-taking, not panic, given high ownership.

Valuation Analysis

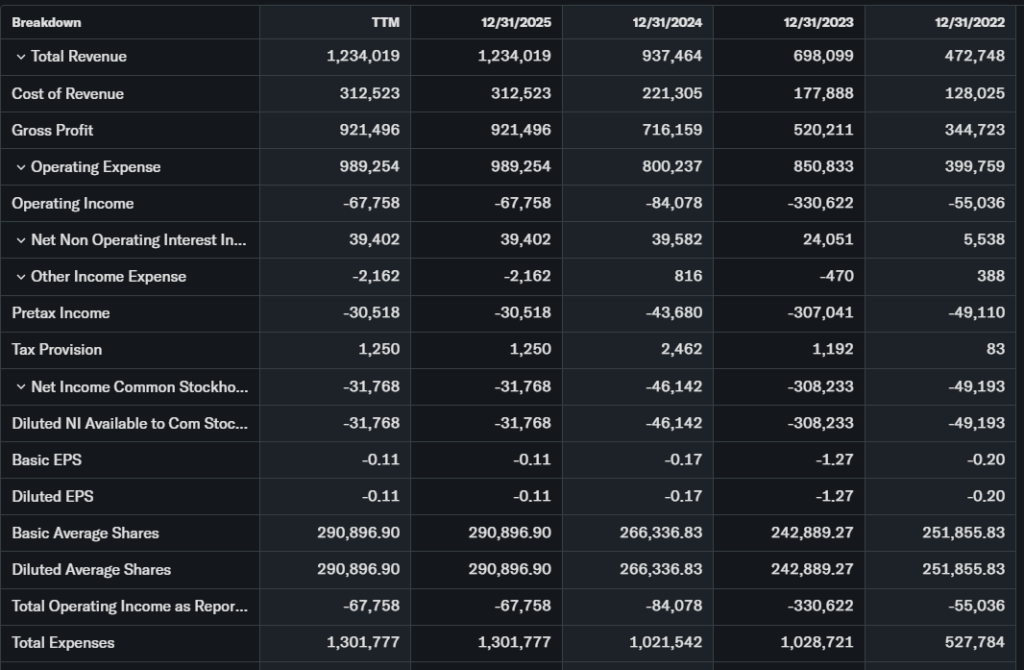

Trailing P/E is negative at -169 due to past losses, but forward P/E is 35.71, reasonable for growth. Price-to-sales around 5x based on $1.23B FY25 revenue.

Revenue grew 32% YoY to $1.234B in FY25; Q4 hit $350.2M, up 30%. EPS improved to $0.19 vs. $0.17 expected. Free cash flow reached $200.4M.

Debt is low with strong cash; non-GAAP margins hit 14%. Vs. Zoom (higher P/E) or Microsoft (mature), KVYO looks fairly valued for its 30%+ growth. Not overvalued.

Recent Earnings & Catalysts

Q4 2025 revenue beat at $350.2M vs. $334M expected, up 29.6% YoY. EPS $0.19 topped $0.17 forecast. FY25 total $1.234B, 32% growth.

Guidance: FY26 revenue $1.501-1.509B, margins 14.5-15%. Catalysts include $500M buyback ($100M accelerated), Google partnership, AI CRM tools, BFCM $3.8B value.

Earnings drove initial pop but stock dipped on macro fears; buyback signals confidence.

Bullish Case

KVYO stock benefits from 30%+ revenue growth and international expansion. AI-driven CRM meets e-commerce demand.

$500M buyback and 27% BFCM gains show operational strength. Rule of 40 score healthy with margins expanding.

Bearish Case

Competition from Braze, Salesforce pressures margins. Slowing macro hits e-commerce spending. Negative net margin -2.57% persists.

Customer churn risk in downturns; 60% yearly drop reflects growth slowdown fears.

Market Sentiment & Investor Psychology

Short interest data limited, but options lean calls post-dip. Institutional ownership high; retail chased the low.

News sentiment above average at 1.9/5. Sentiment neutral to optimistic on fundamentals despite fearful price action.

Short-Term Outlook

Technicals show oversold RSI and volume spike. Momentum may lift to resistance $21-22 if buyback news sustains.

Watch market rebound; expect volatility but potential bounce.

Medium to Long-Term Outlook

Strong business model in AI CRM, industry growth to $10B+. Competitive edge in data platform.

Financial health solid with FCF; hold for long-term investors, accumulate on dips. Risks balanced by 25%+ growth forecast.

FAQ Section

Is KVYO stock a buy right now?

Yes for growth investors; Strong Buy rating, oversold technicals, $42 target. Weigh risks.

What is the KVYO stock price target?

Average $42.40, low $35; implies 100%+ upside from $20.

What are KVYO earnings highlights?

Q4 revenue $350M (+30%), FY25 $1.23B (+32%); FY26 guide $1.5B.

KVYO forecast for 2026?

25-26% growth expected; analysts see rebound.

Major risks for KVYO stock?

Competition, macro slowdown, insider sales.

Suggestions

- Compare with Opendoor analysis

- See our Microsoft stock forecast

- Read our tech sector valuation breakdown

Final Balanced Conclusion

Hold KVYO stock for now; watch for break above $22. Strong growth and buyback offset near-term risks, but macro clarity needed. Long-term accumulation viable.

Disclaimer: This article is for informational purposes only and not financial advice.