Explore SNOW stock analysis with latest price, earnings beat, technicals, valuation, and forecast. Is SNOW stock a buy? Get balanced insights for investors.

Introduction

Snowflake Inc. provides a cloud-based data platform. It helps companies store, manage, and analyze data easily. Investors watch SNOW stock closely after its recent earnings beat. Tech stocks face pressure from high interest rates and AI competition. Yet, data cloud demand grows steadily.

SNOW stock price has swung amid market volatility. Broader conditions like economic slowdowns hit growth stocks hard. Still, Snowflake’s AI integrations draw interest.

Latest Stock Price & Trend

SNOW stock closed at $156.71 on February 26, 2026, after earnings. It rose 5.06% in the last day from recent lows. The 5-day trend shows volatility, up about 9% weekly amid post-earnings moves.

Over one month, SNOW gained 19.64%, recovering from dips. Three-month performance improved from earlier weakness, up amid tech rebound. Six-month trend mixed, with year-to-date up roughly 67% from lows.

The 52-week range spans $120.10 low (April 2025) to $280.67 high (November 2025). Overall trend leans bullish short-term post-earnings, but sideways longer-term. This signals rebound potential for investors, yet caution on resistance.

Technical Analysis

Support levels sit near $150-155, where buyers stepped in recently. These act as floors; breaks signal weakness. Resistance looms at $170-180, capping gains until broken.

RSI at 28.2 shows oversold conditions—below 30 means potential bounce as selling exhausts. MACD line below signal indicates bearish momentum, but watch for crossover.

The 50-day moving average hovers above the 200-day, a bullish sign. No recent golden cross, but no death cross either. Trading volume spiked post-earnings, above average, supporting momentum.

Analyst Ratings & Price Targets

Analysts give SNOW a Strong Buy consensus from 31 Buy, 3 Hold, 0 Sell ratings. Average price target is $272.10, with high at $440 and low $170. This implies 73% upside from $156.

Recent views stay positive despite volatility. Wall Street firms like those on TipRanks see growth in data cloud. Upgrades followed earnings beats. Sentiment suggests confidence, but targets vary on execution.

Insider Activity

Insiders sold 60.74K shares worth $10.35M in last 30 days. No recent buys reported. This follows a pattern of net selling over months.

Large transactions by executives signal caution, perhaps profit-taking at highs. Yet, high institutional ownership at 71% shows long-term faith. Activity implies mixed confidence.

Valuation Analysis

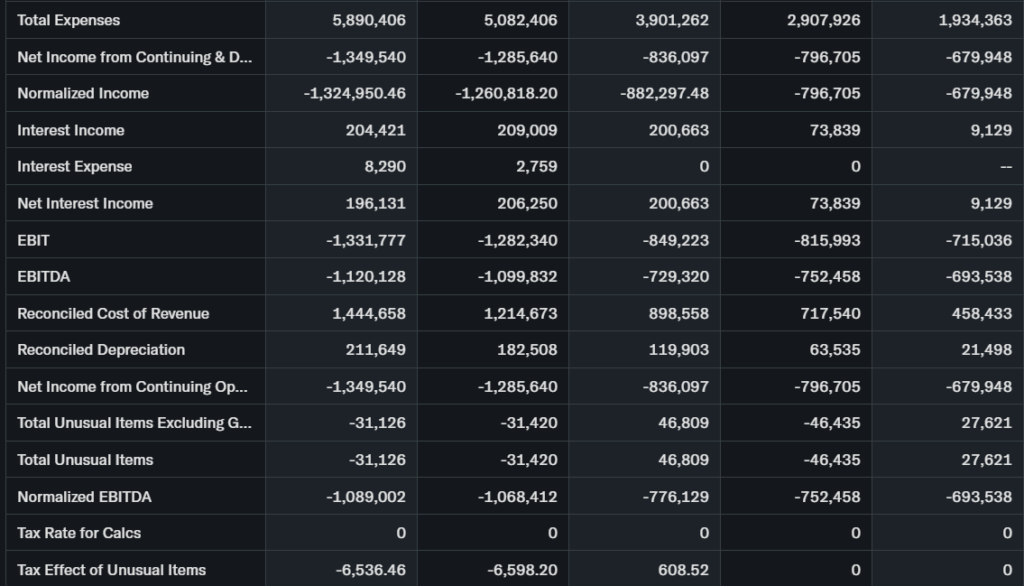

SNOW has no trailing P/E due to losses, but forward P/E is 126.52. Price-to-Sales at 13.91, forward 11.19. Revenue grew 30.1% YoY to $1.28B in Q4 FY2026.

EPS hit $0.32 non-GAAP, beating estimates. Free cash flow strong, but high P/FCF at 80.32. Debt low, cash solid. Compared to peers like Zoom (lower growth) or Microsoft (profitable scale), SNOW looks premium-valued, not undervalued.

Recent Earnings & Catalysts

Q4 FY2026 revenue hit $1.28B, up 30%, beating by 2.42%. Product revenue $1.22B, EPS $0.32 vs. expected -$0.10. Guidance positive on AI tools.

Stock dipped post-earnings despite beats, on high expectations. Catalysts include AI integrations, partnerships. These drive usage growth.

Bullish Case

Data warehousing demand fuels revenue. AI features boost platform stickiness. 30% YoY growth shows momentum. Operational efficiencies improve margins over time.

Market expansion in enterprises supports upside. Tech advantages in cloud data keep edge.

Bearish Case

Competition from AWS, Azure pressures market share. Growth may slow in macro downturn. Margin squeezes from investments. Customer churn risk in economic uncertainty. Regulatory scrutiny on data privacy looms.

Market Sentiment & Investor Psychology

Short interest at 10.75M shares, down 5.78%, days-to-cover 2.0. Options show bullish calls in recent sweeps. Institutional ownership 71%, steady.

Retail piles in post-earnings. Sentiment neutral to optimistic, value bias emerging from oversold.

Short-Term Outlook

Technicals show oversold RSI rebound potential. Volume supports momentum. Momentum favors gains to resistance if market holds. Watch $170 break.

Medium to Long-Term Outlook

Strong business model in data cloud. Industry grows with AI. Competitive moat solid, finances healthy. Hold for long-term investors; accumulate on dips. Risks include competition.

FAQ Section

Is SNOW stock a buy right now?

Strong Buy ratings, but high valuation warrants caution. Wait for pullback.

What is the price target for SNOW stock?

Average $272, high $440, low $170. Upside potential noted.

What are major risks for SNOW stock?

Competition, slowing growth, high multiples.

SNOW earnings next quarter?

Expected EPS -$0.09, watch guidance.

SNOW forecast long term?

Positive on AI data growth; hold/watch.

Suggestions

Compare with Opendoor stock analysis

See our Microsoft stock forecast

Read our cloud tech valuation breakdown

Final Balanced Conclusion

Hold SNOW stock. Earnings strength and technicals support rebound, but valuation and insider sales suggest caution. Watch for guidance execution.

Disclaimer: This article is for informational purposes only and not financial advice.