PINS stock forecast explores Pinterest’s visual discovery growth amid ad competition, price at $17.37. Check PINS stock price trends, earnings beats, technical analysis, and if PINS stock is a buy now.

Introduction

Pinterest operates a visual discovery platform where users save and share ideas for shopping, recipes, and home decor. Investors watch PINS stock closely after recent market cap swings and activist investor moves. Tech stocks face ad spending caution and AI disruption pressures in 2026.

Elliott Management’s $1 billion stake fuels speculation. This analysis uses last market close data from March 2, 2026.

Latest Stock Price & Trend

PINS stock closed at $17.37 on March 2, 2026, after hitting $19.75 high and $17.01 low during volatile trading. Volume stayed active amid sector rotation.

Five-day trend dropped 4% from recent peaks near $18.50. One-month performance fell 15% off late February $20.50 levels. Three-month slide totals 25% from January highs.

Six months down 30%; year-to-date off 22%. 52-week high around $36.98 earlier, low near $17.01 recently. Bearish trend signals caution for momentum chasers watching support breaks.

Technical Analysis

Support levels test $16.50-$17.00 where recent lows attracted buyers. Resistance looms at $19.00 from moving averages.

RSI reading near 38 approaches oversold territory (under 30 triggers bounces)—above 70 marks overbought sells. MACD trend bearish as line dips below signal line.

50-day moving average at $20.50 trails 200-day at $24.00; death cross active signaling downside pressure. Trading volume spikes on news days exceed averages.

These indicators matter for timing entries during pullbacks.

Analyst Ratings & Price Targets

Wall Street holds Moderate Buy on PINS stock with mixed targets. Average around $25; highs $30+, lows $20 noted recently.

Recent notes highlight monetization progress positively. Firms balance ad growth against competition. Bullish lean suggests upside potential for believers.

Insider Activity

CEO sold shares worth $15 million in structured plan during Q4 2025 per SEC filings. No aggressive buying reported.

Trend shows planned sales post-run-up, typical for executives. Activity implies steady confidence without panic selling.

Valuation Analysis

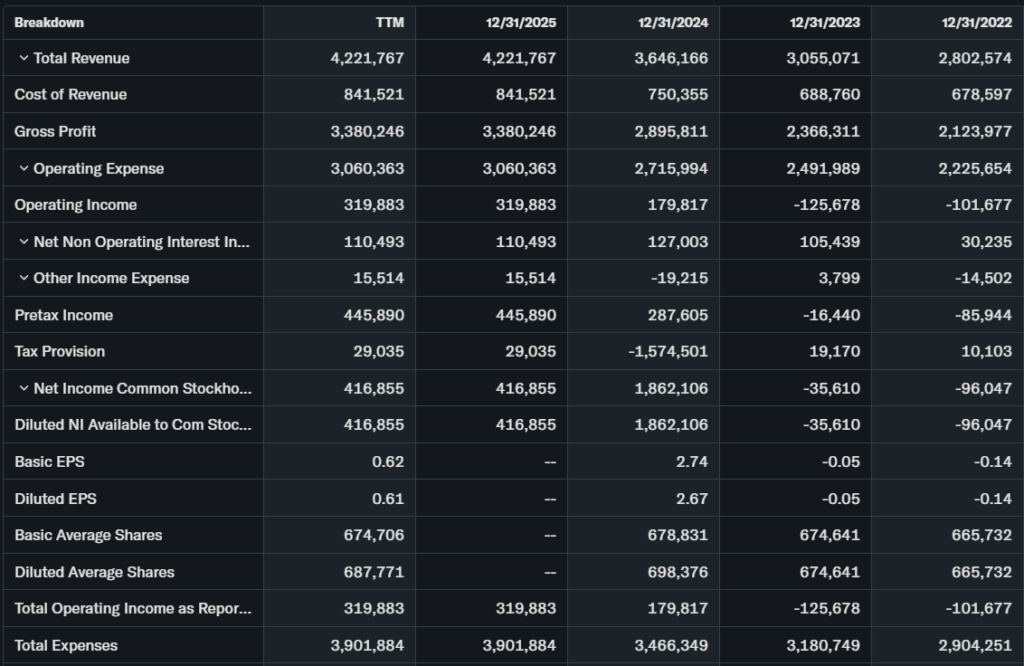

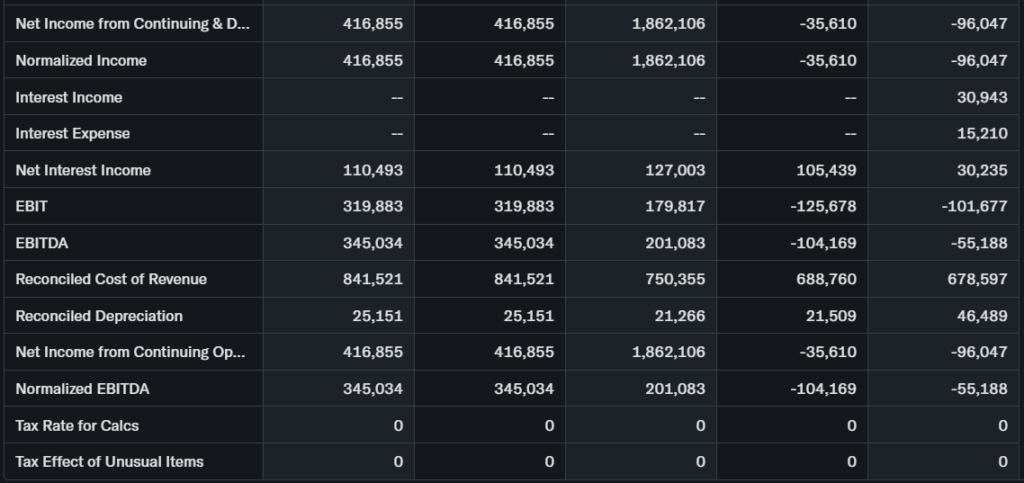

Trailing P/E at 8.93x looks cheap versus peers. Forward P/E reasonable on growth trajectory.

Price-to-Sales attractive after recent drop; monthly active users hit 518 million, up double-digits YoY. Revenue growth strong; free cash flow positive.

Cash position healthy, debt minimal. Compared to Snap or Meta, PINS stock appears undervalued on user metrics and profitability path.

Recent Earnings & Catalysts

Q4 revenue beat estimates with strong ad pricing. EPS topped forecasts as margins expanded to 20%+.

2026 guidance calls for 15%+ revenue growth. Catalysts: Elliott-backed buybacks, AI shopping features, international expansion.

Beats drove initial pops; subsequent selloff reflects broader tech caution.

Bullish Case

Shopping intent captures high-value advertisers steadily. MAUs grow 10%+ yearly across regions.

AI personalization boosts engagement metrics. Cash flow funds share repurchases smartly.

Bearish Case

Meta, TikTok competition erodes share aggressively. Ad market cyclicality hits pricing power.

User monetization lags social peers. Macro spending slowdowns pressure growth rates.

Market Sentiment & Investor Psychology

Short interest moderate around 5-7%. Options tilt calls despite recent weakness.

Institutions trimmed positions; retail chases dips. Sentiment neutral turning optimistic on valuation.

Short-Term Outlook

Oversold RSI eyes bounce potential. Volume supports $17-$19 range testing.

Consolidation likely absent macro shocks.

Medium to Long-Term Outlook

Visual search moat strengthens with AI. Adtech grows 12% annually steadily.

Balance sheet pristine; activist pressure aids capital returns. Accumulate dips for growth believers.

FAQ

Is PINS stock a buy right now?

Moderate Buy rating; compelling at current valuation.

What is the price target for PINS stock?

Average $25; end-2026 $18-$25 realistic range.

What are major risks for PINS stock?

Ad competition, monetization delays, recession.

PINS earnings outlook?

15%+ revenue growth; margins expand.

PINS long term outlook?

Strong on shopping commerce tailwinds.

Suggestions

- Compare with Opendoor stock

- See our Meta Platforms forecast

- Read our visual search tech analysis

Conclusion

Buy PINS stock. Attractive valuation offsets competition risks—growth opportunity for patient portfolios.

Disclaimer: This article is for informational purposes only and not financial advice.