Explore SMCI stock analysis with latest price trends, earnings beats, technical indicators, and 2026 forecast. Is SMCI stock a buy? Get balanced insights for investors.

Introduction

Super Micro Computer (SMCI) builds high-performance servers and storage systems tailored for AI, data centers, and cloud computing. Investors watch SMCI stock closely due to its key role in the AI boom. Broader market conditions, like tech sector volatility and AI infrastructure demand, shape its path.

Latest Stock Price & Trend

SMCI stock closed near $32.27 at last market check on February 27, 2026, after trading in a $28–$35 range in early 2026. It fell from $103.80 in April 2024, hit mid-$40s by late 2025, and stabilized around $29.30 year-end 2025. The one-day performance showed minor gains near $31.65 on March 2, 2026, within a daily high of $31.29 and low of $30.47.

Over five days, it consolidated in the low $30s with low volatility. The one-month trend stayed sideways in the $30–$35 band post-earnings. Three-month and six-month trends leaned bearish from $60 highs in 2025, down sharply from triple-digit peaks earlier. Year-to-date in 2026, it’s flat to slightly up from $29.30, with a 52-week high near $103 and low around $28.

This sideways-to-bearish trend signals caution for short-term traders but potential value for patient investors eyeing AI recovery.

Technical Analysis

Support levels sit at the classic pivot near $30.20, with stronger S1 at $26.70 if breached. Resistance starts at R1 $32.60, then R2 $36.10 on upside breaks. RSI at 52 on the 14-day chart shows neutral momentum, neither overbought (above 70) nor oversold (below 30)—a balanced state that avoids extreme signals.

MACD trend appears weak with ADX near 13, indicating no strong bullish or bearish direction yet; watch for crossovers signaling momentum shifts. The 50-day moving average hovers at $30.90, 200-day at $41.70—stock trades above short-term but below long-term averages, hinting at consolidation. No golden cross (50-day over 200-day) or death cross occurred recently; volume trends stay moderate, supporting range-bound action without breakout conviction.

These indicators matter as they help beginners spot entry/exit points based on price momentum and crowd behavior.

Analyst Ratings & Price Targets

Public.com tracks 13 analysts at consensus Hold, with average 12-month price target $42.38, ranging from Strong Buy to Strong Sell. Futunn pegs average at $39.50, blending AI growth bets with valuation risks. Recent upgrades note margin potential in data center solutions.

Wall Street firms balance AI server demand against volatility; Hold rating suggests steady but not aggressive buying. For investors, this implies limited upside soon but room if earnings deliver.

Insider Activity

CEO and CFO made insider purchases recently, signaling confidence amid AI revenue ramps. No major selling noted in early 2026 reports; transactions lean toward buying in the $30 range. This pattern implies management sees undervaluation, boosting long-term holder sentiment without short-term hype.

Valuation Analysis

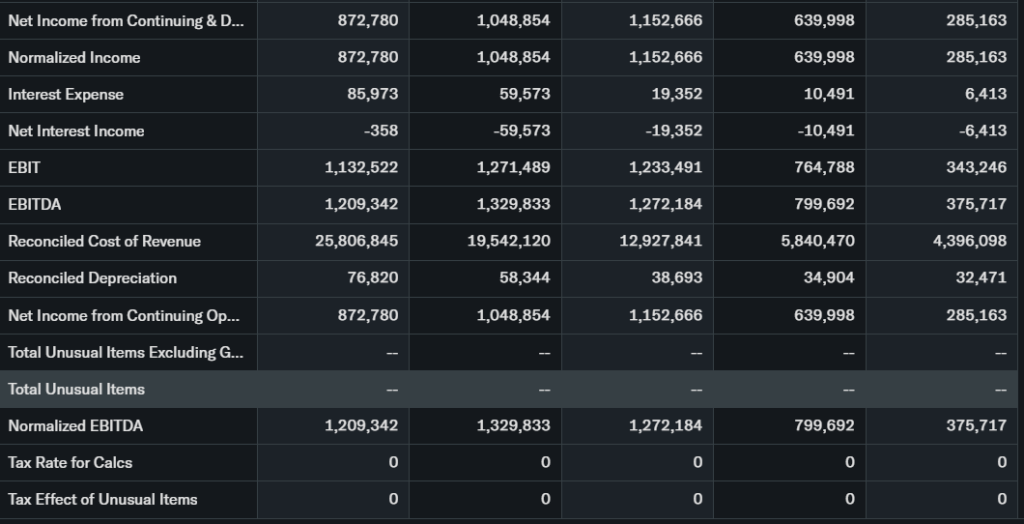

Trailing P/E stays elevated post-growth, but forward P/E factors in FY2026 guidance. Price-to-sales reflects AI focus, with Q2 revenue at $12.7 billion (123% YoY growth). EPS hit $0.69, beating forecasts, though non-GAAP gross margin slipped to 6.4% from 9.5%.

Revenue growth shines at 82% implied for full FY2026 to $40 billion minimum. Free cash flow supports expansion; debt position manageable with strong cash from AI orders. Compared to peers like larger server players, SMCI trades at a discount on forward sales but premium on margins—appears fairly valued, not deeply undervalued yet.

Recent Earnings & Catalysts

Fiscal Q2 2026 delivered $12.7 billion revenue, up 123% YoY, crushing estimates. EPS of $0.69 topped forecasts; guidance raised FY2026 sales to at least $40 billion, over 90% from AI platforms. Margins narrowed, pressuring shares short-term.

Catalysts include new blade servers, AI data center platforms with chip partners, and AI-RAN support announced March 2, 2026. Earnings sparked initial rally but pullback on margin worries, showing mixed stock reaction.

Bullish Case

AI server demand drives revenue, with 123% Q2 growth and $40 billion FY2026 guide. Liquid-cooled racks and partnerships position SMCI for data center buildouts. Operational scale from hyperscalers adds tailwinds without overreliance on one customer.

Bearish Case

Margin compression to 6.4% flags pricing and cost risks in competitive AI hardware. High-beta nature ties to tech sentiment; customer concentration and economic slowdowns could slow orders. Regulatory scrutiny on AI adds caution.

Market Sentiment & Investor Psychology

Short interest data limited, but options show balanced calls/puts amid volatility. Institutional ownership steady; retail chases post-earnings dips. Zacks notes rising attention, with value score aiding momentum shift.

Sentiment leans neutral—optimistic on AI but fearful of margins and macro pressures.

Short-Term Outlook

Technicals point to $30–$36 range with neutral RSI and low ADX. Volume lacks breakout push; market momentum favors sideways hold near supports. Expect consolidation unless catalysts like AI news spark moves.

Medium to Long-Term Outlook

Strong AI model and 82% growth guide favor accumulation for long-term investors. Industry tailwinds in sovereign AI and edge computing help, but competition watches needed. Financial health solid—hold or watch for dips under $30.

FAQ Section

Is SMCI stock a buy right now?

Hold consensus fits current valuation; buy on dips if AI catalysts hit.

What is the price target for SMCI stock?

Average $39.50–$42.38 in 12 months, per analysts.

What are major risks for SMCI stock?

Margin squeezes, competition, and tech volatility top concerns.

What is SMCI earnings outlook?

FY2026 revenue at least $40 billion, EPS growth from AI.

SMCI stock forecast for 2026?

Modest upside to $40s if growth holds, per targets.

Suggestions

- Compare with Opendoor stock analysis

- See our AMD stock forecast

- Read our AI tech sector valuation

Final Balanced Conclusion

Hold for now—AI growth and insider buys support upside, but margins and trends warrant caution. Watch Q3 earnings for conviction.

Disclaimer: This article is for informational purposes only and not financial advice.