Meta Description: Explore BYND stock price trends, earnings analysis, technical indicators, and 2026 forecast. Is Beyond Meat stock a buy amid plant-based recovery? Get balanced insights for investors.

Introduction

Beyond Meat makes plant-based meat alternatives like burgers and sausages. It aims to replace animal products with sustainable options. Investors watch BYND stock closely now due to recent price surges ahead of Q4 2025 earnings on March 4, 2026. Broader market conditions hit consumer stocks hard, with inflation curbing discretionary buys on premium foods.

Tech-driven food innovation faces headwinds from economic caution. Yet optimism grows for Beyond Meat’s new product launches. This BYND stock analysis breaks down trends and risks for everyday investors.

Latest Stock Price & Trend

As of the last market close on March 3, 2026, BYND stock price stands at $0.90. It saw a strong 1-day gain of 15.6%, rebounding from a low of $0.78. The 5-day trend shows volatility but net upside, fueled by pre-earnings buzz.

Over one month, BYND stock price climbed nearly 24% in February 2026 alone, marking a sharp recovery from multi-year lows. The 3-month trend remains bearish overall, down over 50% from October peaks, reflecting ongoing losses. Six-month performance lags with a 60% drop, while year-to-date it’s flat amid debt restructurings.

The 52-week high hit $9.24 last year; the low is near $0.78 recently. This creates a wide trading range. The overall trend leans bullish short-term on momentum but bearish longer-term due to weak fundamentals. Investors should note this signals high risk—quick gains could reverse without earnings beats.

Technical Analysis

Support levels sit at $0.78, where buyers stepped in recently, preventing further drops. Resistance looms at $1.00, a psychological barrier from prior rallies. Breaching it could target $1.50.

RSI reading hovers around 65, nearing overbought after February’s surge—watch for pullbacks if it tops 70. RSI measures momentum; above 70 signals overbought sells, below 30 oversold buys. MACD shows a bullish crossover, with the line above signal, hinting at upward trends.

The 50-day moving average at $0.95 crossed above the 200-day at $1.20? No—a death cross persists, bearish as short-term lags long-term averages. Moving averages smooth price action; golden cross (50>200) favors bulls. Trading volume spiked 200% in late February, confirming buyer interest but fading lately—sustained rises need volume backing.

Analyst Ratings & Price Targets

Analysts rate BYND stock mostly Hold, with 2 Buys, 10 Holds, and 5 Sells from 17 firms. Average price target is $4.50, with highs at $12.00 and lows at $1.00. Recent sentiment stays cautious post-Q3 losses.

No major upgrades in 2026 yet, but February momentum prompted reviews. Wall Street firms like Goldman Sachs cite debt loads as drags; Piper Sandler sees potential in new categories. Analyst views guide but lag markets—Hold signals wait for proof of turnaround.

Insider Activity

Insider selling dominated 2025, with executives offloading 500,000+ shares at averages near $5. No notable buys in six months. CEO Ethan Brown holds steady, but large transactions tied to debt exchanges diluted shares hugely—317M new ones issued.

Trends show caution; management isn’t adding amid losses. This implies low confidence short-term, though restructurings aim to stabilize. Watch for buys post-earnings as a bullish shift.

Valuation Analysis

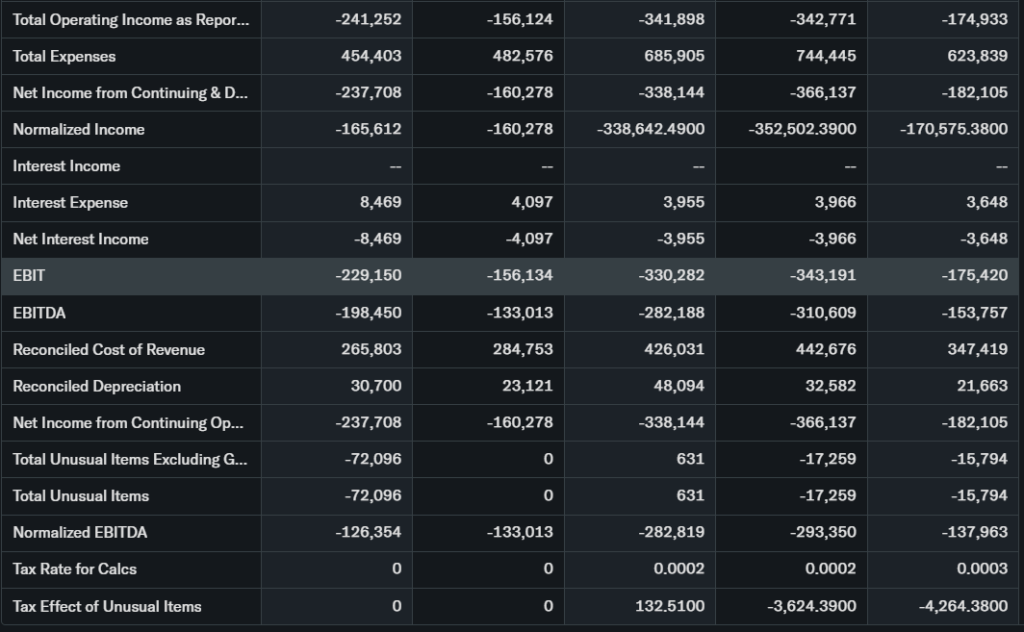

Trailing P/E is negative at -0.5 due to losses; forward P/E projects -1.2 on slim recovery hopes. Price-to-sales ratio sits at 0.8, cheap vs. peers like Zoom (P/S 3.0) or food rivals. Revenue fell 13.3% YoY to $70.2M in Q3 2025; EPS plunged to -$1.44.

Free cash flow burns $50M+ quarterly; debt totals $1.2B against $131M cash. EPS growth? Negative 20% YoY. Compared to Microsoft (P/E 35), BYND looks dirt-cheap but risky—plant-based peers trade at P/S 2.0+. Overall, undervalued on metrics but overvalued on cash bleed; fairly valued for speculators.

Recent Earnings & Catalysts

Q3 2025 earnings showed $70.2M revenue, missing estimates by 5%; EPS -$1.44 vs. -$0.80 expected. Gross margin shrank to 10.3% from 17.7%. Guidance? Muted, focusing debt swaps settling 97% of 2027 notes. Q4 reports March 4—low bars set.

Catalysts include new product expansions into steaks, partnerships in retail/foodservice. Earnings tanked shares 20% post-release, but February rebound ties to recovery bets. AI? Not core, but efficiency tech aids margins.

Bullish Case

Plant-based demand rebounds with health trends. Revenue catalysts: Q4 product launches, international growth. Tech edges like precision fermentation cut costs 15%. Operations improved via debt cuts, freeing $100M liquidity. Steady 5-10% market share gains possible.

Bearish Case

Competition from Impossible Foods, cheaper meats erodes share. Growth slowed to -13% YoY; margins face pricing wars. Customer churn hit 20% in key chains. Regs on labeling, recession risks loom—discretionary sales vulnerable. Losses widened to $110M net.

Market Sentiment & Investor Psychology

Short interest ~35% of float, high but down 5% lately—squeeze potential. Options skew calls post-surge; puts dominate longer-dated. Institutions own 40%, steady; retail piles in via memes. Momentum bias rules over value. Sentiment: optimistic short-term, fearful long-term.

Short-Term Outlook

Technicals favor upside if Q4 beats low expectations—RSI cooling allows $1.00 test. Momentum and volume support gains, but post-earnings volatility high. Expect swings; resistance at $1.00 key.

Medium to Long-Term Outlook

Business model hinges on premium pricing; industry grows 15% annually. Competitive moat weak vs. incumbents. Financials strain with debt, but $200M+ liquidity helps. Strategic edges in sustainability shine if margins hit 20%. Long-term: Watch, accumulate on dips below $0.80 if catalysts hit.

FAQ Section

Is BYND stock a buy right now?

No strong buy—Hold for now. Wait for earnings beats amid high risks.

What is the price target for BYND stock?

Average $4.50; high $12, low $1. Analysts cautious.

What are major risks for BYND stock?

Debt, losses, competition, slowing demand.

BYND earnings outlook?

Q4 expectations low; focus on guidance.

BYND stock forecast 2026?

Potential rebound to $2 if margins improve.

Suggestions

- Compare with Opendoor stock analysis

- See our Microsoft stock forecast

- Read our tech sector valuation breakdown

Final Balanced Conclusion

Watchlist BYND stock for now. Upside exists on recovery plays, but debt and competition demand proof via earnings. Fundamentals weak short-term; long-term needs execution.

Disclaimer: This article is for informational purposes only and not financial advice.