Micron Technology (MU) stock analysis covering price trends, earnings, valuation, and technical outlook for investors wondering if MU stock is a buy.

Introduction

Micron Technology (MU stock) designs and manufactures memory and storage chips used in smartphones, PCs, data centers, and AI hardware. Its DRAM and NAND chips are key ingredients for everything from cloud servers to gaming consoles.

Investors are focused on MU stock now because of a big rebound since late 2025, driven by tight memory supply and surging AI‑related demand. At the same time, broader tech shares have been volatile as interest‑rate expectations and AI‑spending cycles shift, making MU stock a high‑beta way to trade the semiconductor cycle.

Latest MU Stock Price & Trend

As of the latest market close on March 3, 2026, MU stock traded around 410–412 dollars per share, with a day‑range roughly between 397 and 417 dollars. Over the past 24 hours, the stock was up about 1–2%, within a single‑session range that reflects typical volatility for a large‑cap tech name.

Looking at the 5‑day window, MU stock has held broadly flat to slightly positive, indicating short‑term consolidation after a strong prior rally. Over the past month, the stock has risen roughly high‑single‑ to low‑double‑digit percentages, reinforced by AI‑chip demand news and positive earnings headlines.

Over three months, MU stock has climbed into the mid‑ to high‑double‑digit range, while the 6‑month return is well above 100%, reflecting the reopening of memory‑price cycles and data‑center/AI build‑outs. Year‑to‑date, MU stock is up more than 100%, far outpacing the S&P 500 and even the broader semiconductor index.

MU’s 52‑week range spans about 61.5 dollars on the low side to roughly 455 dollars on the high, showing an extremely wide band driven by the AI‑hype cycle and inventory swings. Overall, the trend is clearly bullish, but the pace of recent gains suggests potential for pullbacks or sideways consolidation in the near term.

Technical Analysis

For MU stock, support levels are areas where buyers tend to step in. Recent support clusters appear around the mid‑300s and the low‑400s, where intraday dips have sometimes bounced. Resistance levels sit near the all‑time high and recent session highs, around 440–455 dollars, where selling pressure has occasionally capped rallies.

The Relative Strength Index (RSI) for MU is generally in the upper‑50s to mid‑60s, which is not yet overbought but suggests the stock is in a strong uptrend rather than oversold. An RSI above 70 is usually considered overbought, so the current reading means MU stock is still “bulled up” but not yet stretched to extreme levels.

The Moving Average Convergence Divergence (MACD) shows positive momentum, with the MACD line above the signal line, indicating a bullish trend in the short to medium term. MU’s 50‑day moving average sits beneath the current price, signaling that near‑term momentum is constructive, while the 200‑day moving average is also well below, reinforcing the long‑term uptrend.

There is currently a golden cross pattern (50‑day crossing above 200‑day) in place, which technical traders often interpret as a bullish longer‑term signal. Trading volume has remained elevated versus historical averages, reflecting active institutional and retail interest, especially around earnings and AI‑related news.

Analyst Ratings & Price Targets

Analyst coverage for MU stock is predominantly positive, with most major firms rating the stock a “Buy” or “Strong Buy.” According to recent summaries, roughly 20–30 analysts cover MU, with the majority in the Buy camp, a smaller group in Hold, and only a handful in Sell.

The average 12‑month MU stock price target is about 345–350 dollars, which is roughly 15–20% below the current price, implying analysts see MU stock as richly valued near‑term despite strong fundamentals. The highest target can be significantly above 400 dollars, while the lowest is well below 300 dollars, highlighting a wide dispersion of views on whether the AI‑memory cycle can sustain the rally.

Several Wall Street banks have recently reiterated or upgraded MU stock, citing strong AI‑server demand, HBM‑and DRAM‑pricing power, and improving margins. Others have taken a more cautious stance, warning that inventory cycles and customer‑spending pull‑backs could weigh on MU earnings in the next few quarters.

Insider Activity

Insider activity for MU stock has been mixed in recent months, combining some opportunistic selling with smaller, but steady, long‑term purchases. Major executives have trimmed holdings at elevated prices, which is common after a sharp run‑up and does not necessarily signal a lack of confidence.

At the same time, some board‑level and management‑level insiders have continued to exercise options and hold shares, suggesting a belief in the company’s long‑term business model. Large individual transactions, when disclosed, cluster around months of earnings or product‑launch news, in line with normal corporate‑governance practices.

Overall, insider activity leans more toward sensible profit‑taking than a broad‑based sell‑off, which is consistent with a bullish but cautious stance on MU stock.

Valuation Analysis

MU stock trades at a trailing price‑to‑earnings (P/E) ratio close to 39–40 times, based on the latest trailing‑twelve‑month earnings. The forward P/E, which uses estimated earnings for the next year, is somewhat lower, around the mid‑20s, depending on the data source.

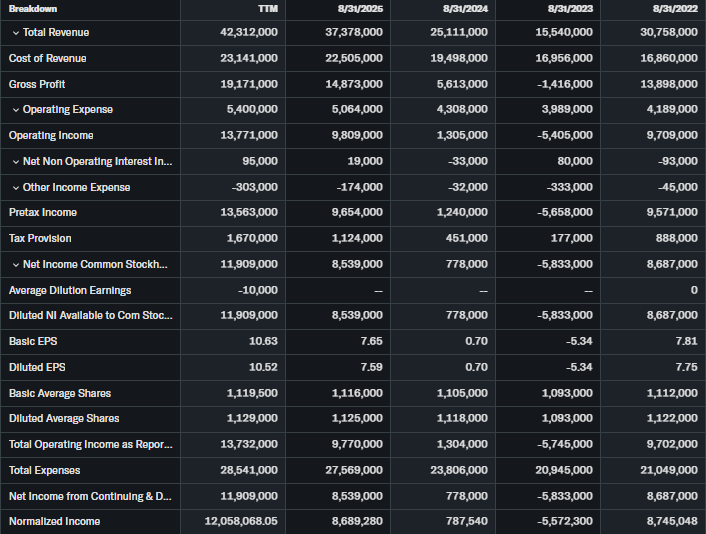

The price‑to‑sales (P/S) ratio is roughly 9–10, reflecting high‑growth expectations for memory shipments and AI‑driven demand. Revenue for the trailing twelve months exceeds 40 billion dollars, with year‑over‑year growth in the mid‑40% range, while net income has surged over 200% versus the prior year.

Earnings per share (EPS) have more than doubled, and free cash flow has improved sharply as utilization and pricing power strengthen. MU carries a relatively modest debt‑to‑equity ratio of around 0.2, with solid cash reserves and strong interest‑coverage metrics, indicating a healthy balance sheet.

On standard valuation measures, MU stock appears closer to overvalued than fairly valued, especially relative to broader semiconductor peers, but its rapid MU earnings growth and AI‑related leverage justify some premium. Compared with firms like memory‑light or diversified tech names, MU’s valuation is elevated, implying that the market has already priced in strong continuation of the memory‑cycle upswing.

Recent Earnings & Catalysts

Micron’s latest quarterly results showed revenue roughly in the mid‑single‑digit‑billion‑dollar range for the quarter, with full‑year revenue approaching 40–42 billion dollars, far above prior‑year levels. EPS also jumped sharply, more than doubling year‑on‑year, as higher ASPs and improved utilization boosted margins.

Both revenue and EPS beat consensus expectations, reinforcing the bullish narrative around HBM and AI‑related DRAM demand. Management’s guidance for the next quarter and fiscal year points to continued growth in data‑center and AI‑focused segments, balanced against some caution on consumer‑end‑market softness.

Key catalysts include ramp‑up of high‑bandwidth memory (HBM) for AI accelerators, new product nodes, and deeper partnerships with cloud and chipmakers. Any signs of oversupply, slower AI‑server adoption, or weaker PC‑and‑mobile demand could conversely weigh on MU earnings and the MU stock price.

Bullish Case

The main bullish argument for MU stock is that AI‑driven data‑center builds and HBM demand will keep memory prices and utilization elevated for several years. As AI clusters require far more DRAM and HBM per server, Micron’s exposure to this structural shift can support strong revenue and margin growth.

The company has also signaled operational improvements, including better cost control, higher‑margin product mix, and more disciplined capex management. If Micron can maintain its technology roadmap and capture market share from competitors, MU stock could continue to benefit from above‑average revenue growth and expanding EPS.

Bearish Case

The main bearish risk for MU stock is a cyclical downturn in memory prices if supply catches up with demand or if cloud customers slow their build‑outs. Historically, semiconductor memory has strong boom‑and‑bust cycles, and even a modest cut‑in‑spending from big data‑center customers could trigger sharp MU stock price declines.

Competition from rivals in DRAM and NAND, along with potential consolidation in the memory industry, could pressure pricing power and margins. Slowing growth in smartphones, PCs, or automotive markets would further erode demand for Micron’s more traditional products, amplifying cyclicality risk.

Market Sentiment & Investor Psychology

Market sentiment on MU stock is currently optimistic but stretched, with high‑beta, momentum‑driven positioning. Retail enthusiasm has been strong, as seen in elevated trading volumes and social‑trading‑platform chatter around MU stock price moves.

Institutional ownership remains substantial, with many large funds overweighting MU as part of their AI‑themed portfolios. Options markets show a tilt toward calls, reflecting a belief that MU stock can grind higher in the medium term, but with sizable downside optionality priced in.

Short‑Term Outlook

Given the bullish technical setup and elevated sentiment, MU stock is likely to remain in an uptrend in the short term, with occasional pullbacks around earnings or macro news. However, the fact that the average price target sits below the current MU stock price suggests that the upside may be limited unless new catalysts emerge.

Trading‑range behavior between recent support and resistance zones is plausible, especially if the broader market encounters volatility. Momentum‑focused traders may continue to ride the trend, while more risk‑averse investors may wait for a better entry closer to support.

Medium to Long‑Term Outlook

Over the next 6–24 months, MU stock’s performance will hinge on whether the AI‑memory cycle sustains or moderates. If demand for HBM and AI‑server DRAM stays strong and pricing power remains intact, the long‑term outlook for MU earnings and MU stock could stay positive.

However, if the cycle cools or oversupply returns, MU stock could experience a de‑rating that brings the MU stock price closer to analysts’ average target. For long‑term investors, MU may be more suitable as a “watchlist” or accumulating‑on‑dips holding rather than an aggressive core position at current levels.

FAQ Section

Is Micron Technology (MU) stock a buy right now?

Many analysts rate MU stock a Buy, but the average price target sits below the current price, suggesting limited near‑term upside unless new catalysts emerge. A cautious, staggered approach may be prudent.

What is the price target for MU stock?

The consensus 12‑month MU stock price target is around 345–350 dollars, implying a modest downside from current levels.

What are major risks for MU stock?

Key risks include memory‑price cyclicality, supply‑demand mismatches, competition, and slower AI‑spending growth, all of which could pressure MU earnings and the MU stock price.

Suggestions

Compare with Opendoor stock

See our AMD stock forecast

Read our tech sector valuation breakdown

Conclusion

MU stock looks best viewed as a high‑growth, high‑beta satellite holding rather than a core low‑risk position at current levels. Given the rich valuation and already‑strong rally, a “hold with watchlist” stance—adding selectively on meaningful pullbacks—may align better with the risk‑reward profile than an aggressive new buy.

Disclaimer: This article is for informational purposes only and not financial advice.