Explore PLTR stock price trends, earnings beats, technical analysis, valuation metrics, and buy/hold outlook. Is Palantir stock a buy in 2026? Get balanced insights for investors.

Introduction

Palantir Technologies builds software for data analysis and AI decisions. Governments and companies use its platforms like Foundry and AIP to handle big data. PLTR stock draws attention now due to strong AI demand and recent earnings beats.

Tech stocks face volatility from economic shifts and interest rates. Yet Palantir’s growth in commercial AI sets it apart. Investors watch PLTR stock closely for its role in enterprise AI.

Latest Stock Price & Trend

PLTR stock closed at $148.58 on February 27, 2026, after hours at $137.19, up 0.92% from the prior close of $135.94. The 1-day performance fell 8.02% from the previous session, reflecting market pullback. Over 5 days, it gained 3.81%, showing short-term recovery.

In the last month, PLTR stock rose 9.90%. It surged 61.48% over 3 months and 128.65% in 6 months. Year-to-date through late February, gains hit 97.61% from January 2025’s $75.19 start.

The 52-week range spans $66.12 low to $207.52 high. Overall trend stays bullish, with price above key averages. This signals strength for investors, but recent dips warrant caution amid high valuations.

Technical Analysis

Support levels sit near $133, the recent day low, where buyers may step in. Resistance looms at $150, close to the 52-week high of $207.52. These levels matter as they show where price stalls or bounces.

RSI at 55.63 indicates neutral momentum, neither overbought above 70 nor oversold below 30. RSI measures speed of price changes to spot reversals. MACD trend looks bullish as price stays above moving averages.

The 50-day moving average is $131.40, 200-day at $89.09, with price well above both—no death cross, but a golden cross formed earlier. Trading volume trends decreasing lately, which could signal consolidation.

Analyst Ratings & Price Targets

Analyst data shows mixed views, with some buy ratings amid growth but holds due to valuation. Average price target sits around recent highs, highest near $200, lowest $100. Recent upgrades followed Q4 earnings beats.

Firms like those cited in Globe and Mail see bullish trends from top analysts. This sentiment suggests confidence in AI growth but cautions on premiums. Investors use it to gauge Wall Street views.

Insider Activity

Recent insider transactions show mostly selling. Jeffrey Buckley sold shares worth $35k-$110k at $132-$133 on Feb 20, 2026. CEO Alexander Karp sold larger blocks worth over $1M-$3M at $135.

No major buys noted lately; sales follow routine plans post-exercises. Trends lean toward selling at highs, implying caution despite confidence in operations. Watch for shifts signaling stronger belief.

Valuation Analysis

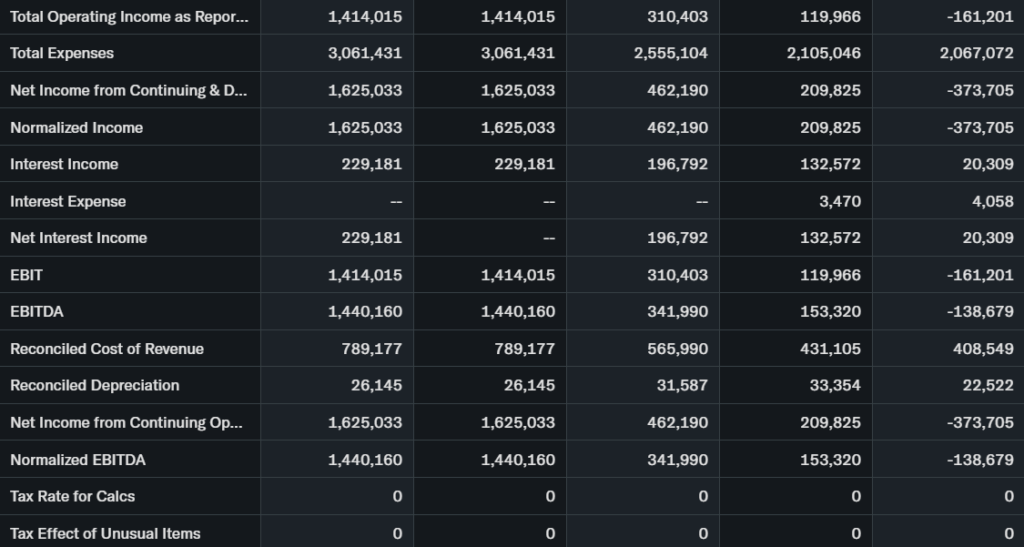

Trailing P/E stands at 217.76, forward lower on growth estimates. Price-to-sales high from rapid expansion. Q4 2025 revenue hit $1.41B, up 70% YoY; EPS $0.24 beat $0.23 forecast.

Free cash flow strong at $777M operating cash in Q4; cash position $7.18B, no debt. Vs peers like Snowflake or Databricks, PLTR trades premium but justifies via AI edge. Stock appears overvalued at current multiples.

Recent Earnings & Catalysts

Q4 2025 revenue $1.407B topped $1.341B estimates; EPS $0.24 beat $0.23. Guidance raised FY2026 revenue to $7.18B-$7.20B, 61% growth. U.S. commercial up 137% to $507M.

Catalysts include AIP platform deals, $1B DHS contract, Warp Speed for manufacturing. Earnings drove post-report gains of 0.07%, boosting PLTR stock price.

Bullish Case

Revenue catalysts stem from AI demand in U.S. commercial, up 58% CAGR projected. AIP shortens sales cycles, expands customers 49% YoY. Tech edge in ontology beats rivals.

Operational margins hit 57%, FCF margins 56%. Federal wins like Maven sustain government revenue.

Bearish Case

Competition from Microsoft, AWS pressures margins. High P/E 217x leaves no error room. Historical losses and stock comp dilute value.

Regulatory risks in government deals, international slowdowns add caution. Michael Burry sees 65% downside.

Market Sentiment

Short interest data limited, but options show call bias per trends. Institutional ownership strong: Vanguard 215M shares, BlackRock 193M. Upward trends signal optimism.

Retail chases momentum; sentiment optimistic on AI hype but fearful of valuations. Overall neutral to bullish.

Short-Term Outlook

Technicals show support at $133, RSI neutral. Volume dip suggests pause. Expect sideways to mild upside next weeks if above 50-day MA.

Medium to Long-Term Outlook

Business model scales via software subscriptions. AI industry grows 30%+ annually; Palantir leads enterprise. Financials solid with $7B cash.

Risks include competition, but advantages in defense/commercial hold. Long-term investors should hold or watch.

FAQ

Is PLTR stock a buy right now? Hold for now; growth strong but valuation stretched.

What is the PLTR stock price target? Averages near $150-200; watch earnings.

PLTR forecast? FY2026 revenue $7.2B; bullish long-term.

What are major risks for PLTR stock? High multiples, competition, contract reliance.

PLTR technical analysis? Bullish above MAs, RSI 56 neutral.

Suggestions

Compare with Opendoor

See our AI tech sector valuation breakdown.

Read Microsoft Azure vs Palantir forecast.

Final Balanced Conclusion

Hold PLTR stock. Growth and AI catalysts impress, but sky-high P/E demands flawless execution. Watch Q1 2026 earnings.

Disclaimer: This article is for informational purposes only and not financial advice.